Provides access to product training, sales and marketing resources, deal registration, and more to our VARs, Integrators, Resellers and other channel partners.

Seagate Technology partnered with ESG to develop custom research to make sense of the growing multicloud complexity and the challenges it poses to business data. The goal of the research was to provide insight to business leaders about how their cloud-savvy peers are using cloud infrastructure to drive innovation while also controlling costs in the cloud—and to gauge the resulting business benefits.

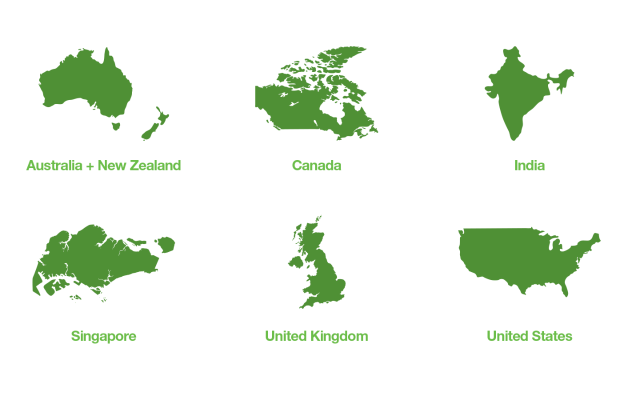

The insights provided by The Multicloud Maturity Report come from a global survey administered in February 2022. The number of survey respondents was 500. Respondents comprised senior leaders in IT (71%) and software development/data analytics (29%). The leaders have influence over their organization’s storage, cloud, and/or data management technology decisions. Their organizations store at least some of their data in the public cloud. They work for small/midmarket (less than 1,000 employees, 24%) and enterprise (1,000+ employees, 76%) organizations—all with at minimum 1PB of unstructured data under management. Multiple industry verticals are represented, including technology, manufacturing, communications and media, and business services among others. The respondents live in Australia, Canada, India, New Zealand, Singapore, the United Kingdom, and the United States.

About ESG

Enterprise Strategy Group, or ESG, is an integrated technology analysis, research, validation, and strategy firm that provides market intelligence, actionable insight, and go-to-market content services to the global IT community. ESG is recognized as one of the world’s most influential technology analyst firms.

Practice Director Scott Sinclair, Senior Analyst Rob Strechay, and Senior Director of Custom Research Adam DeMattia led the survey project and analysis at ESG.

About Seagate

Seagate Technology crafts the datasphere, helping to maximize humanity’s potential by innovating world-class, precision-engineered, mass-data storage and management solutions with a focus on sustainable partnerships. A global technology leader for more than 40 years, the company has shipped over three billion terabytes of data capacity.

Multicloud is a mess—and, more likely than not, your organization’s data must make the best of it. At a time when IT organizations are extra concerned about their budgets, it’s crucial to both minimize costs and maximize innovation. This report provides a plan for how to do it.

Drawing on an original global survey of senior IT and business leaders, the report constructs a unique Multicloud Maturity Model depicting the growing multicloud complexity. More importantly, it equips business leaders with specifc steps they can take today to navigate the mix of clouds in a way that controls data costs and accelerates innovation. The survey reveals that following these steps results in tangible benefts: companies that score high on multicloud maturity see greatly improved valuations, faster time to market, and the ability to beat revenue goals.

Introduction

No Such Thing as the Multicloud (Yet)

We live in a world of accelerating innovation, much of which depends on business leaders wielding dizzying sets of new tools, services, and cost models. Not to mention the ecosystem in which data, the currency that powers innovation, moves—the multicloud.

What is the multicloud?

If you ask Seagate CIO and EVP of Storage Services Ravi Naik, he’ll say that “in ideal terms, the multicloud is the ability for data workloads to be migrated on and off clouds and among different clouds in a frictionless manner and as needed—with no lock-in, no concern of throttling, and no penalties for pulling data off and moving workloads around.”

“But,” he’ll caution, “this world doesn’t exist today.”

In this sense, there is no such thing as the multicloud—yet.

There are only multiple clouds. The various cloud repositories of the multicloud ecosystem raised tall walls around them. Data can get in easily; leaving is another story. The clouds do not freely talk to each other. This system makes it diffcult for organizations to choose one platform today and a better platform tomorrow.

Ironically, the resulting lock-in paralyzes the very thing for which a multiplicity of clouds are built—data. And it impedes the business value that this data contains.

The multicloud ecosystem too often alienates business leaders from their own organizations’ data.

A Data-Centric, Realistic Lens

Today, a variety of approaches are used to ascertain multicloud complexity. A report like this could concern itself with the full stack or end-to-end benchmarks of multicloud maturity. There are other industry leaders that take such strategies and do it well.

For over four decades now, Seagate has been a data-centric company. It should not be a surprise then that this report and the survey we commissioned apply a data-centric lens. The survey is designed to refect the too-often missed primacy of data to modern enterprise business strategy.

Like it or not, multicloud strategy is often imperative to enable data-centric business value. It is the context in which business data lives, the air that data breathes.

Much as the idealists among us may wish for one single cloud, for most companies that is far from reality. The muliticloud is not going away anytime soon. (When we use the term muliticloud in this report, we mean the multiplicity of clouds that aren’t great at communicating and tend to lock in data.) Our investigation takes this messy multicloud reality as a given. We fnd it useful to ask how enterprises can best support their underappreciated business currency—data—in its current context.

The survey on which this report is based shows clearly that what businesses do with their data matters. It makes a difference to outcomes, such as revenues, profts, net promoter score, the ability to meet budgetary goals, and even the valuation of a company.

Invariably, companies that scale successfully are the ones that put data at the core of all they do. The most mature multicloud strategies are data-centric strategies.

Enlarge

Section 1

Key Findings

Multicloud complexity is on the rise.

Business data moves and lives among a mess of clouds and is subject to the friction brought by poor communication among them.

A majority (82%) of respondents already use 2+ public cloud infrastructure service providers (excluding Software as a Service, or SaaS). This fgure is expected to increase to 93% in two years

A great deal of momentum is taking place among those using 4+ cloud infrastructure providers: 30% of respondents today. The Multicloud Maturity survey shows that this number will more than double in two years, rising to 63%.

More than half of the respondents (53%) represent organizations currently managing 100+ intercloud integrations. The estimated mean among digital native organizations is ~145, and among other organizations ~107 (i.e., digital natives manage 36% more integrations).

Not surprisingly, 76% of survey takers say monitoring, measuring, and ensuring service-level agreement (SLA) adherence for applications that rely on intercloud integrations is challenging.

Data costs further exacerbate the ecosystem’s complexity.

They contribute to data lock-in and, ultimately, impede innovation.

84% of respondents agree the opportunity exists for their organization to better leverage its existing data to create business value.

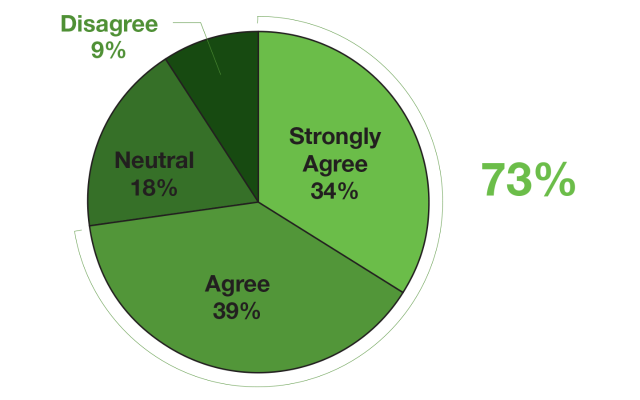

But 73% report that their organization is hampered by data retention costs, which limits their ability to maximize data value.

The friction built into today’s multicloud need not be the status quo.

The survey points to a way out.

The survey that informed this report constructs a Multicloud Maturity Model. The model examines how companies score on two fronts—minimizing data costs and maximizing data-driven innovation. The survey aggregates the two scores into a macro maturity model.

The model is one of a kind in considering data-driven costs and innovation in the multicloud and to relate performance on these fronts to business outcomes.

The high-level question that ESG and Seagate asked is this: Do organizations that control data-related costs and scale data-driven innovation in the multicloud see meaningful business value as a result?

The higher the total multicloud maturity, the better the business rewards.

The answer to the above question is a resounding yes. Organizations that score high on both fronts produce measurably better business outcomes.

Companies that are most adept at navigating the multicloud in terms of costs and innovation are 5.3× more likely than their peers to beat revenue goals by 10%.

Organizations scoring high on multicloud maturity are 6.3× more likely to go to market months or quarters ahead of their competition.

The higher the total multicloud maturity, the better the business rewards.

The answer to the above question is a resounding yes. Organizations that score high on both fronts produce measurably better business outcomes.

Companies that are most adept at navigating the multicloud in terms of costs and innovation are 5.3× more likely than their peers to beat revenue goals by 10%.

Organizations scoring high on multicloud maturity are 6.3× more likely to go to market months or quarters ahead of their competition.

The survey ties the data cost and innovation stories to forward-looking valuation.

The aggregate value of what a company is worth. By excelling at data costs and innovation in the multicloud, organizations are much better positioned to win more business value.

Leaders in multicloud maturity were 3.2× more likely to forecast their valuation 3 years from now will be 5× or greater than it is today.

He report spells out how to get to higher maturity.

Last but not least, the survey also asked: What are the multicloud maturity leaders doing with their data that others can learn from? The report lists specifc steps that companies can take no matter where they place on the multicloud maturity spectrum.

Section 2

A Jumble of Clouds: Multicloud Complexity

It makes sense to follow industry convention in speaking about the multicloud in the singular (as if it were a coherent whole). Equally it makes sense to be realistic: as we noted earlier, there is no such thing as a unifed, well-functioning multicloud (yet). There are only multiple clouds—a jumble of clouds that, frankly, have a hard time communicating. This reality, as this report will show, poses risk to the value businesses can derive from their data.

The survey underpinning this report gives testimony to the growing friction that data moving among the clouds encounters: multicloud complexity. To say that the complexity of the multicloud ecosystem is intensifying these days is an understatement.

Before delving into the survey results illustrating the complexity, let’s briefy acknowledge the context for all this: data is, of course, growing at an astounding rate. Any and all available sources confrm this. According to ESG’s Multicloud Maturity survey, the median three-year compound annual growth rate (CAGR) for unstructured data under management is 39.4%. Seagate’s 2020 Rethink Data report noted that enterprise data, which grows faster than consumer data, was expected to have an average annual growth rate of 42%. This corresponds to other research documenting the staggering growth of the datasphere (that is, the totality of data created, consumed, and stored in the world).

“The Global DataSphere is expected to more than double in size from 2022 to 2026,” according to John Rydning, research vice president of IDC’s Global DataSphere program. “The Enterprise DataSphere will grow more than twice as fast as the Consumer DataSphere over the next fve years, putting even more pressure on enterprise organizations to manage and protect the world’s data while creating opportunities to activate data for business and societal benefts.” According to the 2022 Global DataSphere forecast report by IDC,

in 2022 enterprises were on track for generating 59 zettabytes (ZB) of data. In 2026, they are forecast to generate 155ZB. All this is part of 221ZB of data that IDC predicts will be generated overall in the global datasphere in 2026.

The world is awash with data. And masses of data need to be going places—at times resting for the short term, and at others coming to stay for good. In many cases, these locations (momentary or long-term) are part of the multicloud ecosystem. And so we arrive at our conundrum.

The Multicloud Maturity survey conducted by ESG renders a reality dense with communication issues. And business leaders are feeling the pain of this friction. The survey fndings detail the swelling complexity:

A majority (82%) of respondents already use 2+ public cloud infrastructure service providers (excluding SaaS). This fgure is expected to increase to 93% in 2 years.

A great deal of momentum is taking place among those using 4+ cloud infrastructure providers: 30% of respondents. The survey showed that this number would more than double in two years, as it was expected to rise to 63%.

The multicloud is sprawling. 87% of respondents think distributed applications will become mainstream over the next two years.

56% of organizations storing hot/warm data—which needs real-time or frequent access—on cloud infrastructure say that data is accessed by applications which run in a different environment on at least a daily basis (though only 12% say continuously).

More than half of the respondents (53%) represent organizations that currently manage 100+ intercloud integrations. The estimated mean among digital native organizations was ~145, and among other organizations ~107 (i.e., digital natives manage 36% more integrations). For the purposes of this survey, ESG and Seagate defned digital natives as organizations “born in the cloud” (meaning, founded in the last 25 years) and investing more than 10% of their revenue toward the research and development of digital products and services.

Not surprisingly, 76% of survey takers say monitoring, measuring, and ensuring SLA adherence for applications that rely on intercloud integrations are challenging.

Both data and troubleshooting intelligence about the data get lost in the multicloud fog. The most frequently reported challenge is the inability to pinpoint the root cause of problems when they are detected (30% of respondents). And 64% of respondents report service-impacting issues on account of intercloud application integration failures at least once a month.

As the next section shows, the complexity of infrastructure results in the often inscrutable and volatile data- related costs, which further intensify friction.

The survey driving this report makes a unique contribution to the existing multicloud explorations by linking data-driven costs and data-driven innovation in the multicloud context. For this purpose, ESG analysts constructed the Multicloud Maturity Model. Organizations were appraised based on specific inputs in areas of multicloud cost maturity and multicloud innovation. The two sets of inputs were then combined into one macro Multicloud Maturity model. This section deals with data cost maturity; the next one examines innovation maturity; and the ensuing section contains insights on the aggregate model that combines both cost and innovation maturities.

The Inputs

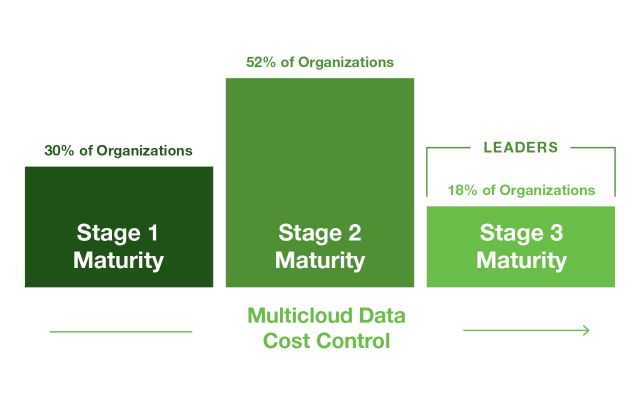

In the area of data-related costs, respondents were placed into one of three groups based on the steps they’ve taken to more effectively manage cloud storage costs.

ESG employed a point-based scoring system. Organizations could earn up to 50 maturity points based on how they answered five questions related to how they manage cloud storage costs:

Does the organization use cloud cost estimation tools/software to help model and compare costs with different public cloud providers and private clouds?

Does the organization rigorously consider workload and data requirements prior to deciding where data will be placed?

Once in the cloud, does the organization monitor data and workload patterns over time?

Has the organization made investments in tools and staffing with an eye toward improving cloud storage costs?

Has the organization automated workflows associated with cloud storage operations?

ESG then segmented organizations based on the total number of points earned. The breakdown of organizations in the research is as follows:

Stage 1 (least mature organizations): 25 or fewer points—30% of organizations represented.

Stage 2 (moderately mature organizations): 25.5-35 points—52% of organizations represented.

Stage 3 (leaders): More than 35 points—18% of organizations represented.

When it comes to multicloud cost control, a variety of challenges loom. The 2020 Seagate report Rethink Data found that only 32% of data available to enterprises is used. We wondered: Were business leaders unaware of the lost opportunity? The Multicloud Maturity survey signals that they are aware of it, but—at least in part—multicloud’s data-related costs get in the way of data value.

84% of respondents agree the opportunity exists for their organization to better leverage its existing data to create business value.

But 73% report that their organization is hampered by data retention costs

(storage media costs, egress costs, API fees, etc.), which limit their ability to maximize data value.

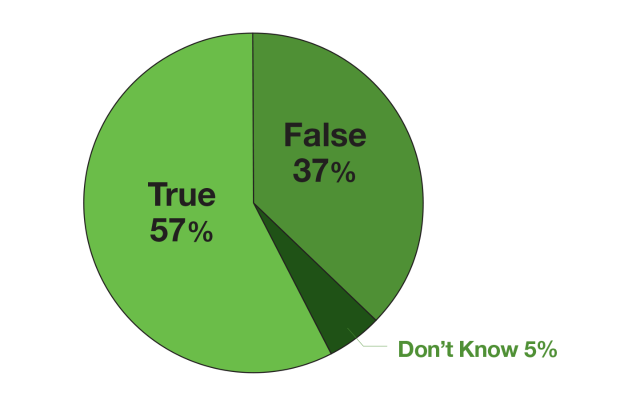

Nearly three fifths of respondents report that data storage costs have caused them to delete data in the past year.

Figure 3. 57% of queried business leaders report deleting what they know to be valuable business data because of prohibitive storage costs. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 1. Multicloud maturity in the area of data-related cost control. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 2. 73% of respondents report that storage costs hamper their organization’s ability to derive value from data. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 3. 57% of queried business leaders report deleting what they know to be valuable business data because of prohibitive storage costs. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 1. Multicloud maturity in the area of data-related cost control. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 1. Multicloud maturity in the area of data-related cost control. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 2. 73% of respondents report that storage costs hamper their organization’s ability to derive value from data. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 3. 57% of queried business leaders report deleting what they know to be valuable business data because of prohibitive storage costs. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 4. Business leaders are feeling the pain related to data costs in the multicloud. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 4. Business leaders are feeling the pain related to data costs in the multicloud. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 4. Business leaders are feeling the pain related to data costs in the multicloud. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 4. Business leaders are feeling the pain related to data costs in the multicloud. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Business leaders aren’t as in charge of their organizations’ own data as they should be:

81% of leaders surveyed say they often incur unexpected cloud costs related to data egress and ingress after a migration.

79% say “timing and budget forecasting is extremely challenging to do accurately.”

And 78% report that they “often incur unexpected cloud costs related to the number of API calls made by applications after a migration.”

The numbers in this section paint a picture of an immensely valuable business currency—data—whose potential is nowhere near reached.

Scaling in the multicloud is hard—and it can exacerbate data storage challenges.

The system appears designed to lock data in.

High egress fees and existing commitments lock data in with a provider and prevent easy movement between environments. It makes it harder for data to go where it is needed, or where it can render its insights.

Data is too often siloed.

Splitting data between environments limits workload portability and increases compliance risks.

Data-related costs are volatile.

Exponential data growth, high costs, and hidden fees substantially increase storage TCO.

Organizations have less control over resiliency and security.

Fragmented systems require companies to double-down on security and resiliency to minimize weak links.

Does greater multicloud maturity around data costs matter all that much? In what ways?

It does pay to be a leader. The survey found that:

Leaders, or Stage 3 organizations, are 3.3× more likely to rate themselves as very effective managing cloud storage costs over time.

The most multicloud-mature organizations reduced their cloud storage costs by 36% (resulting in overall capacity savings that are 77% greater than Stage 1 organizations).

Leaders are 3.9× more likely to be very confident in their future-facing cloud spending forecasts.

How do non-leader organizations inch closer to full multicloud maturity? The good news is that no matter where an organization places on the maturity model, there are steps it can take to improve its cost- related multicloud prowess. The following spider web chart shows how leaders differed from less mature organizations, providing some clues.

Enlarge

How Does Your Organization Measure Up?

To gauge how your organization would score on multicloud cost control maturity, ask yourself the following questions.

Do you use third-party cloud cost estimation tools?

Yes, always

Yes, sometimes

No

Which requirements do you carefully evaluate before determining where to store data?

Performance/latency requirements

Location/network bandwidth available for users

Availability requirements

Data access and mobility (e.g., ingress/egress)

API calls

Which characteristics does your organization monitor continuously over time?

Performance/latency

Network connections of users

Availability

Ingress/egress of data

API calls

Which investments has your organization made in the last 12 months to help effectively manage cloud storage costs?

Tools that provide comprehensive visibility over all cloud storage usage

Hiring more staff

Funding training and certification of employees

Storage platforms that are cross-environment compatible

Application re-architecture projects

Automation tools

How automated are each of the following tasks for cloud storage at your organization today?

Monitoring data flows

Provisioning and updating end-user access permissions

Protection of data (i.e., backup, retention, archive)

Enforcing data security (e.g., encryption)

To compare your answers with how maturity leaders did, take a look at page 15, including the spider web chart. And for ideas on how your organization can do better, see the advice in the following section.

ESG Recommendations

Scaling in the multicloud is hard—and it can exacerbate data storage challenges.

Use a predictive third-party cloud cost tool.

Leverage tools that help measure the cost of cloud resources for every deployment decision. Leaders were 12× more likely to utilize third-party cloud cost estimation tools every single time when making a data placement decision. Stage 1 organizations were far more likely to either say they do not leverage third-party cloud cost estimation tools or that they do—but only for some of the time.

Consider deployment criteria.

Prior to deploying applications, evaluate multiple requirements—such as performance, availability, data mobility, API, and user network bandwidth—to ensure that your application will be able to deliver the expected user experience. Leader organizations not only evaluated twice as many deployment criteria as Stage 1 organizations on average, but they were also far more likely to look at availability and API requirements in their evaluation. Moving applications is costly and complex. Do sufficient upfront analysis to ensure that your app will deliver as expected.

Monitor characteristics.

Once applications are up and running, continue to monitor the environment to ensure that the requirements or capabilities do not change over time. Leader organizations monitored almost twice as many application characteristics—such as performance, availability, data mobility, API, and user network bandwidth— than Stage 1 organizations on average. Leader organizations were also 2.3× more likely monitor the user network capabilities than Stage 1 organizations. This suggests that in order to ensure the right user experience organizations need to monitor both the application environment and the user environment.

For investment, prioritize tools in addition to training.

To ensure that your organization continues to effectively manage your cloud costs, invest in the right tools as well as training. Both Stage 3 and Stage 1 organizations were relatively similar in their investments in training and additional staff. But leaders (Stage 3) were far more likely to invest in tools and technology, such as automation tools, visibility tools, or storage platforms that are cross-environment compatible. For example, most mature organizations were 3.1× more likely than Stage 1 to invest in tools that offer comprehensive visibility across their multicloud environment.

Automate security and protection.

Digital businesses benefit from the accelerated operations that result from the increased use of automation. Automate processes to reduce the burden on personnel as much as possible. Leaders automated more than twice as many functions—such as monitoring data flows, the provisioning and updating of end-user access permissions, the protection of data, and the enforcing data security—than Stage 1 organizations on average.

“When trying to prove the connection between actions and outcomes with research, you never really know if your hypothesis will be borne out. In this case, it is clear that an organization’s actions move the needle both on cloud costs and innovation outcomes. It’s unique how the combination of both taking action on cloud costs and promoting innovation with cloud ops can lead to a dramatic impact on the health of the business.”

In addition to cost control, the Multicloud Maturity survey looked at organizations’ ability to scale innovation. As part of the Multicloud Maturity Model, respondents were asked for specific inputs in areas of both multicloud cost maturity and multicloud innovation. The two sets of inputs were then combined into one macro Multicloud Maturity Model. The previous section deals with data cost maturity; this one examines innovation maturity; and the following section combines the two types of multicloud maturity into a macro model and ascertains business results.

The Inputs

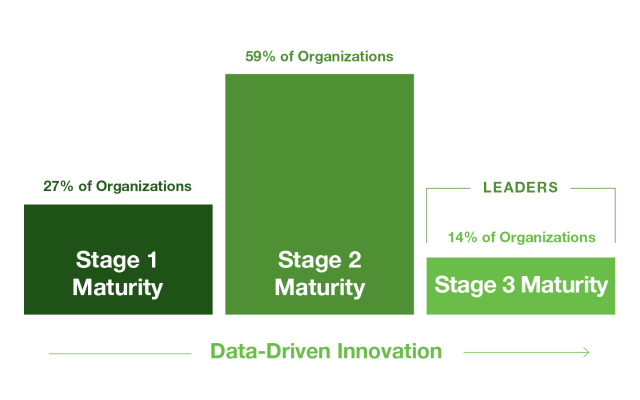

In the area of data-driven innovation, respondents were placed into one of three groups based on the steps they’ve taken to more effectively use cloud technologies to drive innovation.

ESG employed a point-based scoring system. Organizations could earn up to 30 maturity points based on how they answered three questions related to how they leverage data in the multicloud to fuel innovation:

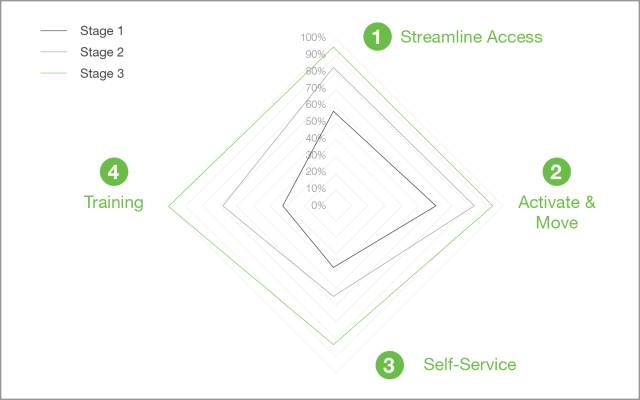

Does the organization streamline access to data and seamlessly move it so innovators can use it without friction?

Does the organization allow data consumers to provision data and infrastructure in a self-service manner?

Does the organization frequently educate data consumers on how to provision data and infrastructure (considering the proper requirements)?

ESG segmented organizations based on the total number of points earned. The breakdown of organizations in the research is as follows:

Stage 1 (least mature organizations): 15 or fewer points—27% of organizations represented.

Stage 2 (moderately mature organizations): 15.5-25 points—59% of organizations represented.

Stage 3 (leaders): More than 25 points—14% of organizations represented.

The survey results are decisive: Organizations that empower data consumers to effectively use the cloud to free up their data for innovation saw meaningfully better business results.

When companies offered streamlined access to data, enabled data’s seamless movement to get data to innovators quickly, enabled self-service for data and infrastructure consumers, and frequently educated data consumers on how to provision data and infrastructure, their businesses thrived.

Here are the most significant findings:

The most multicloud-mature organizations (in the area of data-driven innovation) are growing data- related revenue 57% faster than their less mature peers.

Stage 3 organizations have launched 2.5× as many products/services reliant on data innovation in the last 12 months.

Leaders are 2.6× more likely to say product innovation is driving higher customer satisfaction (CSAT).

They are 2.8× more likely to have strengthened their competitive position.

They are 2.2× more likely to have grown customer wallet share.

Stage 3 organizations are 6.3× more likely to go to market months or quarters ahead of their competition.

What the survey makes clear is that it is not enough for businesses to amass data. Data alone is not insight. A non-negotiable for converting data into insight is access—easy, quick, built-in access to data for its intended users. Without access, there is no insight. Without insight, there can be no innovation.

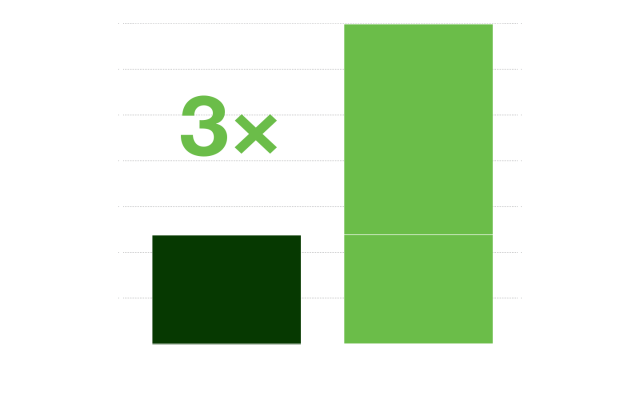

To wit: The survey found that the most innovation-mature organizations are 3× more likely to get data in the hands of developers significantly faster than they did 12 months ago.

Finally, those working for the most innovative companies express much greater enthusiasm for their organizations as measured by the net promoter score (NPS). NPS measures customer loyalty, satisfaction, and positive impression. It answers the question, “On a scale from 0 to 10, how likely are you to recommend this company to a friend or colleague?”

We wanted to find out what kind of NPS feedback is common for the IT organization among the data users within companies that invest in the most in data-driven innovation.

Figure 6. Multicloud maturity in the area of data-driven innovation. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 6. Multicloud maturity in the area of data-driven innovation. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 6. Multicloud maturity in the area of data-driven innovation. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 6. Multicloud maturity in the area of data-driven innovation. Distribution of organizations (n=500). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 7. Multicloud maturity in the innovation area translates directly to the ability to get the data into the hands of innovators significantly faster. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey.nAll rights reserved.

Figure 7. Multicloud maturity in the innovation area translates directly to the ability to get the data into the hands of innovators significantly faster. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey.nAll rights reserved.

Figure 7. Multicloud maturity in the innovation area translates directly to the ability to get the data into the hands of innovators significantly faster. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey.nAll rights reserved.

Enlarge

Figure 7. Multicloud maturity in the innovation area translates directly to the ability to get the data into the hands of innovators significantly faster. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey.nAll rights reserved.

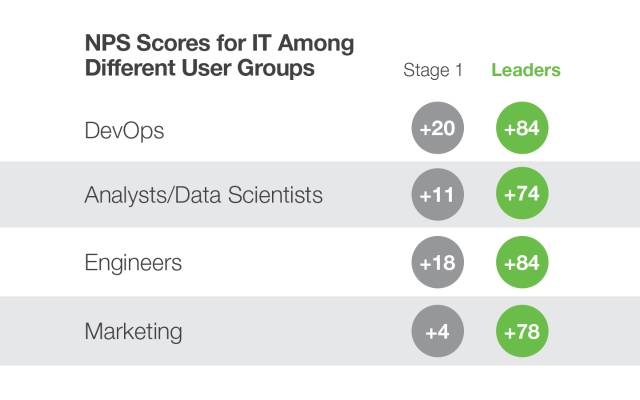

The survey shows that maturity leaders’ IT organizations enjoy significantly higher NPS. Those working for the most innovative companies express comparatively much greater enthusiasm for their IT teams (see Figure 8).

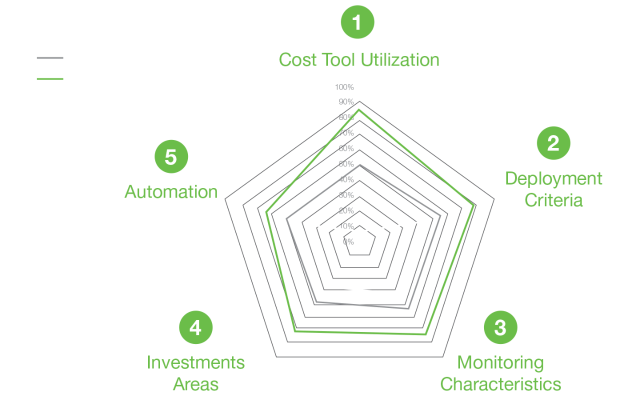

Given the clear benefits of investing in data-driven innovation, what are the ways for non-leaders to punch above their weight? Much like with multicloud cost maturity, the good news is that no matter where an organization places on the maturity model, there are steps it can take to improve its data-driven innovation results. The following spider web chart depicts how leaders differed from less mature organizations.

Figure 8. Members of DevOps, analytics and data science, engineering, and marketing departments rave about IT organizations that make data access easy. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved

Figure 8. Members of DevOps, analytics and data science, engineering, and marketing departments rave about IT organizations that make data access easy. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved

Figure 8. Members of DevOps, analytics and data science, engineering, and marketing departments rave about IT organizations that make data access easy. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved

Enlarge

Figure 8. Members of DevOps, analytics and data science, engineering, and marketing departments rave about IT organizations that make data access easy. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved

Enlarge

How Does Your Organization Measure Up?

To determine how your organization would score in the area of multicloud maturity related to scaling innovation, ask these four questions.

How would you rate the technologies, processes, and skills in place to streamline data access to innovators?

Very strong

Good, but room to improve

Work in progress or weak

How would you rate the technologies, processes, and skills in place to activate data and seamlessly move it to where it needs to be?

Very strong

Good, but room to improve

Work in progress or weak

What proportion of data consumers can provision data and infrastructure for their projects in a self- service manner?

100% of data consumers

61% to 99% of data consumers

41% to 60% of data consumers

21% to 40% of data consumers

0% to 20% of data consumers

How often do you conduct training and knowledge sharing with data consumers to help them understand, request, and provision data and infrastructure with a technology profile that matches workload requirements?

Quarterly or more often

Twice per year

Once per year

Less often than once per year

Don’t know

To compare your organization with how the leaders did, take a look at pages 20 and 21, including the spider web chart. And for ideas on how your company can level up, turn to the advice in the following section.

ESG Recommendations

Leveling Up: What You Can Do

Streamline access.

Leaders are 4.2× more likely to identify as “very strong” in this area. This is where measuring your perception and your internal customers’ perception of how well they access the data will be key. Take it group by group, step by step. Select, for example, the data scientists—and explore with them how you can get them to the point where they confirm that they have the access they need at least 80% of the time.

Invest in tech that seamlessly moves data.

The multicloud-mature organizations are 2.6× more likely to identify as “very strong” on this front. Focus on the right data moving to the right place at the right time. This could be using multiple technologies, from very sophisticated application service mesh to orchestrated secure file transfer protocol. There is no need to jump straight into a cloud-native way of moving data seamlessly. You can make progress by looking for the data path of least resistance. And remember that you must take into consideration data governance and country regulations.

Accelerate access with self-service.

On average, leaders provide 2.1x as many of their data consumers with the ability to access data and infrastructure in a self-service manner. A significant gap exists in this area between leaders and Stage 1 organizations. Allowing different data consumers to see and use data on their own will greatly increase their ability to innovate and therefore their satisfaction, leading to higher NPS scores. Look for a tool to aid you on the self-service journey. Of course, there is not a one-size-fits-all tool. A tool effective for data scientists will not fit well for marketing groups. So, pick a persona as a starting place and build out from there.

Train early, often, and invest in collaboration.

Leaders are 16.7× more likely to offer quarterly (or more frequent) training, which highlights the importance of combining tools and tech with skills investment. Education can lead to acceptance and better usage of the data infrastructure. This might be a good first place to start by not only leveraging IT resources, but also partnering with outside departments. You will also learn from building these pieces of training some of the gaps that exist for particular data consumer groups within your organization.

Measure the NPS of data consumers.

NPS of data users are up to 9× higher among multicloud-mature organizations compared to Stage 1 organizations. Measure the NPS and, if it’s not high, follow up with questions and action. You can’t manage what you can’t measure. It is important to at least start with a self-assessment NPS. This means arriving at a number for each of the groups you service with data on how well they think you satisfy their needs with data. This becomes the baseline for other points of action.

“Scaling data innovation takes putting together a plan to execute over time. In my experience at a major hyperscaler and several startups, I learned that you must work backward from the data user. Put a name to the persona, fully understand the needs of that persona for data, and talk to them to understand what the gaps are today. Then understand that the strategy has to unfold in stages—no “big bang” all at once—and set expectations with a roadmap that first crawls, then walks, and finally runs to data innovation.”

Rob Strechay

Senior Analyst, ESG

The next section brings cost control and innovation maturities together. What business results are enjoyed by organizations that score well on both? Let’s find out.

Section 5

The Multicloud Maturity Model

How organizations that excel at both managing cloud costs and fostering innovation outperform their peers

Multicloud maturity is only as good as the benefits it offers. What good would it be, after all, if in the end the revenues and valuations of the mature organizations remained at the level of their less mature peers?

A key question driving this survey was: Do organizations scoring high on both cost control and fostering innovation see any tangible results? Adding up maturity in the areas of cost minimization and maximizing innovation rendered a macro maturity model that answers this question.

First, a word on how the fully multicloud-mature companies were identified.

Organizations could earn up to 50 points for practices aimed at managing multicloud costs and up to 30 points for fostering cloud innovation (see previous two sections). ESG analysts segmented organizations based on their total multicloud maturity points earned by adding their scores from both cost and innovation areas.

The aggregate allows us to ascertain the correlation between comprehensive cloud practices—spanning cost management and scaling innovation—and overall business performance.

The overall multicloud maturity scale breaks down as follows:

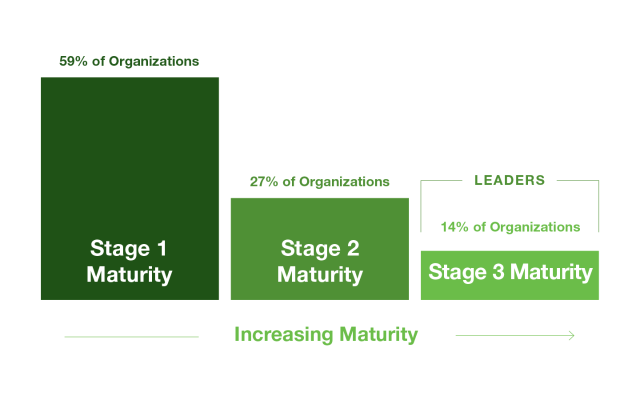

Stage 1 (least mature organizations): 50 or fewer points—59% of organizations represented.

Stage 2 (moderately mature organizations): 50-59.5 points—27% of organizations represented.

Stage 3 (leaders): More than 60 points—13% of organizations represented.

“When trying to prove the connection between actions and outcomes with research, you never really know if your hypothesis will be borne out. In this case, it is clear that an organization’s actions move the needle both on cloud costs and innovation outcomes. It’s unique how the combination of both taking action on cloud costs and promoting innovation with cloud ops can lead to a dramatic impact on the health of the business.”

Adam Demattia

Senior Director of Custom Research, ESG

The aggregate allows us to ascertain the correlation between comprehensive cloud practices—spanning cost management and scaling innovation—and overall business performance.

The overall multicloud maturity scale breaks down as follows:

Stage 1 (least mature organizations): 50 or fewer points—59% of organizations represented.

Stage 2 (moderately mature organizations): 50-59.5 points—27% of organizations represented.

Stage 3 (leaders): More than 60 points—13% of organizations represented.

Figure 10. Comprehensive Multicloud Maturity Segmentation. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 10. Comprehensive Multicloud Maturity Segmentation. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 10. Comprehensive Multicloud Maturity Segmentation. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 10. Comprehensive Multicloud Maturity Segmentation. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

ESG analysts determined that 13% of organizations performing best on both cost and innovation fell into the most multicloud-mature category (a.k.a Stage 3 or leaders).

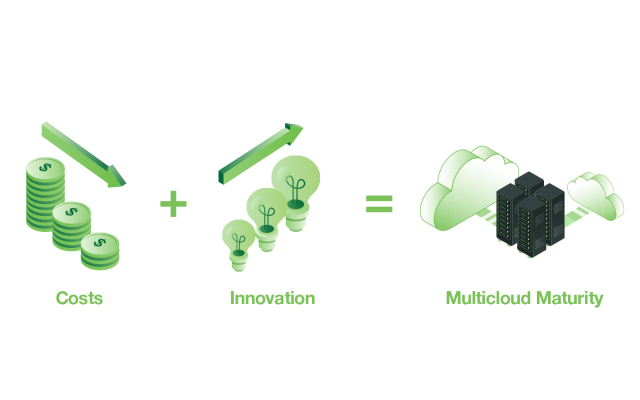

The formula for multicloud maturity is the following:

Enlarge

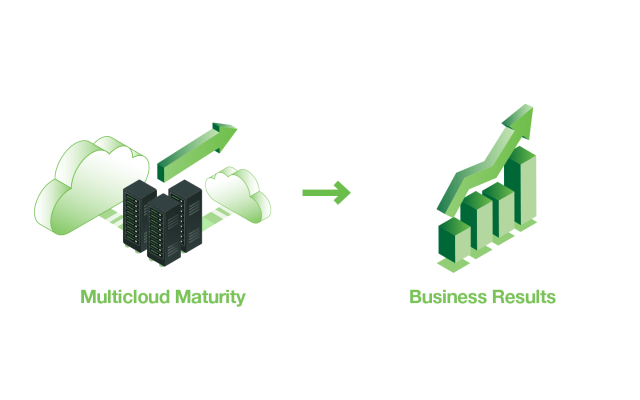

What do we know about the business results that this exclusive, most multicloud-mature club enjoys?

The higher the total multicloud maturity, the higher the business rewards.

Organizations that best manage cloud costs and foster innovation with the cloud outperform their peers at a business level. In particular, they:

Beat their revenue goals by nearly twice as much as their less mature counterparts.

Are almost 3× more likely to report that their organization is in a very strong business position.

Are more than 3× more likely to expect their companies’ valuation to increase fivefold over the next 3 years.

Enlarge

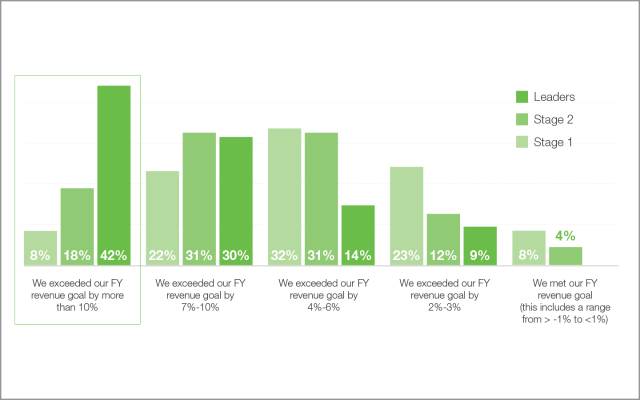

Figure 11. High-maturity organizations (Stage 3) tend to overperform their most recent fiscal year revenue goals by almost twice as much as the least mature organizations (Stage 1). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 11. High-maturity organizations (Stage 3) tend to overperform their most recent fiscal year revenue goals by almost twice as much as the least mature organizations (Stage 1). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 11. High-maturity organizations (Stage 3) tend to overperform their most recent fiscal year revenue goals by almost twice as much as the least mature organizations (Stage 1). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 11. High-maturity organizations (Stage 3) tend to overperform their most recent fiscal year revenue goals by almost twice as much as the least mature organizations (Stage 1). ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

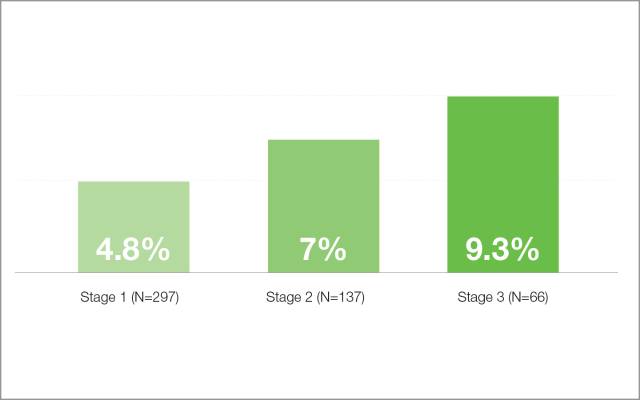

Remarkably, the multicloud maturity leaders are 5.3× more likely than the other organizations to beat their revenue goals by more than 10%.

Figure 12. High-maturity organizations are 5.3× more likely to have beaten their revenue goals by more than 10%. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 12. High-maturity organizations are 5.3× more likely to have beaten their revenue goals by more than 10%. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 12. High-maturity organizations are 5.3× more likely to have beaten their revenue goals by more than 10%. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 12. High-maturity organizations are 5.3× more likely to have beaten their revenue goals by more than 10%. ® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Given how well the top mulitcloud performers did on the revenue front, it follows that more of those organizations report greater confidence when it comes to the future of their business.

Figure 13. High-maturity organizations are nearly 3× more likely to report that their organizations are in a very strong business position.

® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 13. High-maturity organizations are nearly 3× more likely to report that their organizations are in a very strong business position.

® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Figure 13. High-maturity organizations are nearly 3× more likely to report that their organizations are in a very strong business position.

® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

Enlarge

Figure 13. High-maturity organizations are nearly 3× more likely to report that their organizations are in a very strong business position.

® 2022 ESG, Inc. The Seagate Multicloud Maturity Survey. All rights reserved.

The takeaway: Taking steps to achieve higher multicloud maturity leads to better business results. The leveling- up strategies shared in sections titled “Assessing Multicloud Maturity: Minimizing Data-Related Costs” and “Assessing Multicloud Maturity: Maximizing Data-Driven Innovation” are well worth implementing.

Cross-Referencing the Leaders on Cost and Innovation

If a company does well on one of the multicloud maturity pillars—say, cost control—is that likely to predispose it to do well in the other area—innovation? The survey identified some connections.

Companies that succeed at minimizing costs tend to do well when it comes to innovation. The reverse is also true—organizations that excel at innovation tend to be ones that know how to control costs. The correlations are clear on both fronts but are stronger for the latter. The leading innovators outcompete their peers partly because of their cost-controlling skills.

When examining top performers on innovation (only), ESG found they perform well in the area of cost minimization in the following ways:

They are 3× more likely to be very effective at managing cloud storage costs over time than Stage 1 organizations.

They have avoided 56% more cloud storage costs than their least multicloud-mature peers.

They are 3.4× more likely than Stage 1 organizations to be very confident that their cloud spending forecasts for the next fiscal year will be accurate.

It’s not a given that when an organization is efficient at cost control (only), it will also excel at innovation. But the survey found that a solid correlation exists between the two. Organizations that outperform others on the cost control front have great results when it comes to innovation in the following ways:

They have launched 57% more services reliant on data innovation in the last 12 months than Stage 1 organizations.

They are 3.7× more likely than their least multicloud-mature peers to report that new products have driven higher customer satisfaction.

They are 3.2× more likely than Stage 1 organizations to report having accelerated the time it takes to deliver data to developers in the last 12 months.

The upshot? If your company is in control of its multicloud costs, it is likely to also be good at promoting innovation. If your organization is great at innovation, it likely got there, in part, thanks to effective cost-saving practices.

Aiming for excellence on both fronts is the multicloud’s holy grail. In an ecosystem rife with impediments, it is a strategy that can free up your data from lock-in, delivering maximum business value.

Conclusion: Less Friction, More Value

Multicloud, as we know it, is a jumble of clouds.

It can be tricky for data to navigate the multicloud ecosystem swiftly, seamlessly, and without getting stuck. This reality should matter to any business leader because data is a conveyor of business value.

As this report makes clear, companies that win are ones that keep down data-related costs while scaling data-driven innovation. From consistently using cloud cost estimation tools to investing in tech that enables easy data movement, organizations can take pragmatic actions to become more mature in supporting their data throughout the multicloud. This report identifies these steps.

In many ways, innovation is about eliminating friction that slows down and locks in data—whether it’s cost- or access-related friction.

Multicloud is, for many organizations, a given. Its many sources of friction? They’re optional.

The good news is that we can reassert ownership of our business data, and win more business value as a result. Regardless of where your company scores on the Multicloud Maturity Model, it can enact the practices used by winning organizations to get more out of data.

These practices, no matter how seemingly small, will free up your data as it makes its journey from creation to insight, from insight to innovation, from innovation to market—and finally from market to greater business value.

The next section brings cost control and innovation maturities together. What business results are enjoyed by organizations that score well on both? Let’s find out.

Data Breakdown by Country

The survey queried senior business leaders from around the globe. The respondents reside in Australia, Canada, India, New Zealand, Singapore, the United Kingdom, and the United States.

Between 91% and 100% of all respondents across every country said their organizations store data across multiple clouds today. The majority of respondents in all markets either strongly agreed or agreed that they often incur unexpected cloud costs related to data egress/ingress after a migration.

As for how they each stand out from the rest, ESG analysts called out a few statistically significant differences. (Australia and New Zealand were combined.)

Take a look:

Enlarge

Australia + New Zealand

Technological inventiveness is embraced by these two countries. Respondents in Australia and New Zealand (ANZ) report that their organizations are leading edge/early majority when it comes to technology adoption (97% vs. 71% for the rest of the world).

Survey takers in ANZ more often agree that their organization is hampered by data retention costs (storage media costs, egress costs, etc.), limiting their ability to maximize data value (94% vs. 72% for rest of the world).

ANZ respondents are more apt to report that pursuing a multicloud storage strategy to achieve long-term business and technology goals is critical (44% vs. 24%).

Underscoring the prior point, while 34% of ANZ-based respondents report their organization uses a single public cloud infrastructure provider today, only 3% expect they will use a single provider 24 months from now.

89% of ANZ-based respondents agree the opportunity exists for their organization to better leverage its existing data to create business value.

Canada

Canadian survey takers more frequently say that hot/warm data hosted in a public cloud is accessed or called by applications that run in a different environment “all the time” (21% vs. 11% for the rest of the world).

Remarkably, despite that, the queried Canadians are less likely to report that their organizations suffer service-impacting issues monthly or more often as a result of a change to an application (e.g., a new code release) that causes an intercloud application integration to fail (46% vs. 66%).

While 62% of Canadian respondents say that their organization is hampered by data retention costs, they were more likely than the rest of the world to report they have not discarded potentially valuable data due to cost over the last 12 months (53% vs. 36% for other countries).

Correspondingly, 91% of Canadian organizations believe that “opportunity exists for their organization to better leverage existing data to create business value.”

In Canada, insufficient support for training data administrators was selected as a top challenge when monitoring, measuring, and ensuring SLA adherence for applications that rely on intercloud integrations (35% vs. 18% in other countries

India

Automation of data protection and security stood out in India. Survey takers were more likely than their peers to report that data protection and security workflows in the cloud have been entirely or mostly automated (68% vs. 49% and 68% vs. 47% respectively).

Indian respondents were more likely to report their investments and processes are very effective at managing cloud storage costs over time (71% vs. 35% for other countries).

The above points show the focus Indian organizations have on data enablement. As to why, Indian respondents were more likely than their peers to strongly agree that the opportunity exists for their organization to better leverage its existing data to create business value (59% vs. 39% in other countries).

Indian business leaders were more likely to say that their organizations’ ability to activate data and seamlessly move it to where it needs to be is very strong (68% vs. 46%).

88% (vs. 78% worldwide) of Indian respondents have registered that it is important or critical to pursue a multicloud storage strategy to achieve its long-term business and technology goals.

Singapore

Respondents were more likely to agree that “opportunity exists for my organization to better leverage its existing data to create business value” (97% vs. 83% for other countries).

Of respondents expecting to use multiple clouds, 94% recognized it is important/critical to pursue a multicloud storage strategy to achieve its long-term business and technology goals.

Automated policy creation is important to Singaporean businesses. Survey takers were more likely to report that their organization had made investments in the past 12 months in automation tools to simplify policy creation and enforcement over data flows, access and permissions, and protection and security to better manage cloud costs (74% vs. 54%).

Respondents in Singapore more often believe that product innovation powered by data had led to their organization improving its brand perception (42% vs. 20% for rest of the world).

Representing a mindset that prizes learning and innovation, survey takers in Singapore were more likely to report investing more than 10% of their revenue back into research and development of digital products/services (74% vs. 56%).

In the last 12 months, Singaporean organizations have made investments in hiring more staff with cloud expertise (35%) and funded the training and certification of employees in cloud expertise (58%) in order to effectively manage cloud storage costs.

United Kingdom

UK organizations are further along on public cloud adoption, on average storing 40% of their data in public cloud environments (vs. 36% in other countries).

Respondents in the UK were also more apt to expect their organization to leverage more than five different CSPs 24 months from now (30% vs. 15%).

UK survey takers reported that more of their workloads leverage cloud-native architectures (40% vs. 32% on average).

UK respondents say that their organizations are leading edge/early majority when it comes to technology adoption (87% vs. 69% for the rest of the world).

88% of UK business leaders believe that their organizations’ adoption of cloud technologies is being somewhat or significantly hindered or slowed by storage cost considerations.

The UK is lagging behind other countries in hiring staff with cloud expertise, only 30% of organizations having done so, the lowest of all countries surveyed (vs. 42% in other countries combined).

The UK companies are wasting a lot of important data. In the past 12 months, 69% of organizations have deleted or discarded unstructured data that could have been used to create business value.

United States

In the United States, business leaders report that their organizations are grappling more with cloud storage costs: they are less likely to say their investments aimed at managing cloud storage costs over time have been very effective (30% vs. 45% for other countries).

The US is also set to have one of the highest growth rates of unstructured data under management over the next three years. On average these respondents forecast a 40% annual growth rate.

Additionally, they are less likely to be very confident in their forecasted cloud spending for the next fiscal year (30% vs. 40%).

US respondents were somewhat less likely to agree that data has the potential to dramatically impact their business: they were less likely to agree their organization can better leverage its existing data to create business value (80% vs. 88%).

US respondents report their organizations are leading edge/early majority when it comes to technology adoption less often than rest of the world (64% vs. 82%).

US companies were less likely to report a host of business benefits tied to data-led product innovation, including being less likely to have: improved customer satisfaction (14% vs. 25%), entered new markets (13% vs. 25%), increased customer wallet share

(14% vs. 22%), and improved brand perception (18% vs. 25%).